By

By

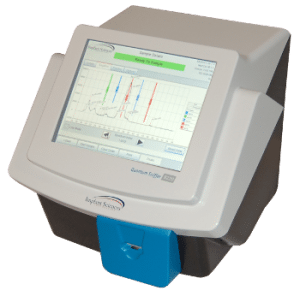

L-3 Communications [LLL] on Monday said it has agreed to acquire the explosive trace detection (ETD) business of Implant Sciences [IMSC] for $117.5 million in cash, a deal which would add a handsome new capability to its Security & Detection Systems division.L-3 will fund the acquisition through cash on hand. Deal terms include the assumption of certain liabilities.Implant on Monday entered Chapter 11 Bankruptcy protection and L-3’s asset purchase agreement is contingent to approval by the U.S. Bankruptcy Court, a…